To achieve AML customer risk rating and scoring, a business will need to start with examining the type of data that exists relevant across all customers and/or the majority of customers.

The data will then need to be examined for relevance to ML/FT risks. This may include information of the country or countries linked to the client either by being domiciled or reach of business activity.

The expected volume of the customer activity and the expected value of the customer activity is also relevant to segregating risks levels.

The types of products or services that the customer accesses should be included in the AML customer risk rating, including the method of interaction with the client.

Where some customers have data gaps, an automatic default of high should be applied to that data gap. Once the ‘missing’ information is gathered, the client’s profile can be updated for the AML customer risk rating model.

AML360™ provides your business with advisory services to develop a compliance framework for AML customer risk rating and reporting. Using regulatory technology we can test the risk methodology for adequacy and application of the AML/CFT risk-based principles.

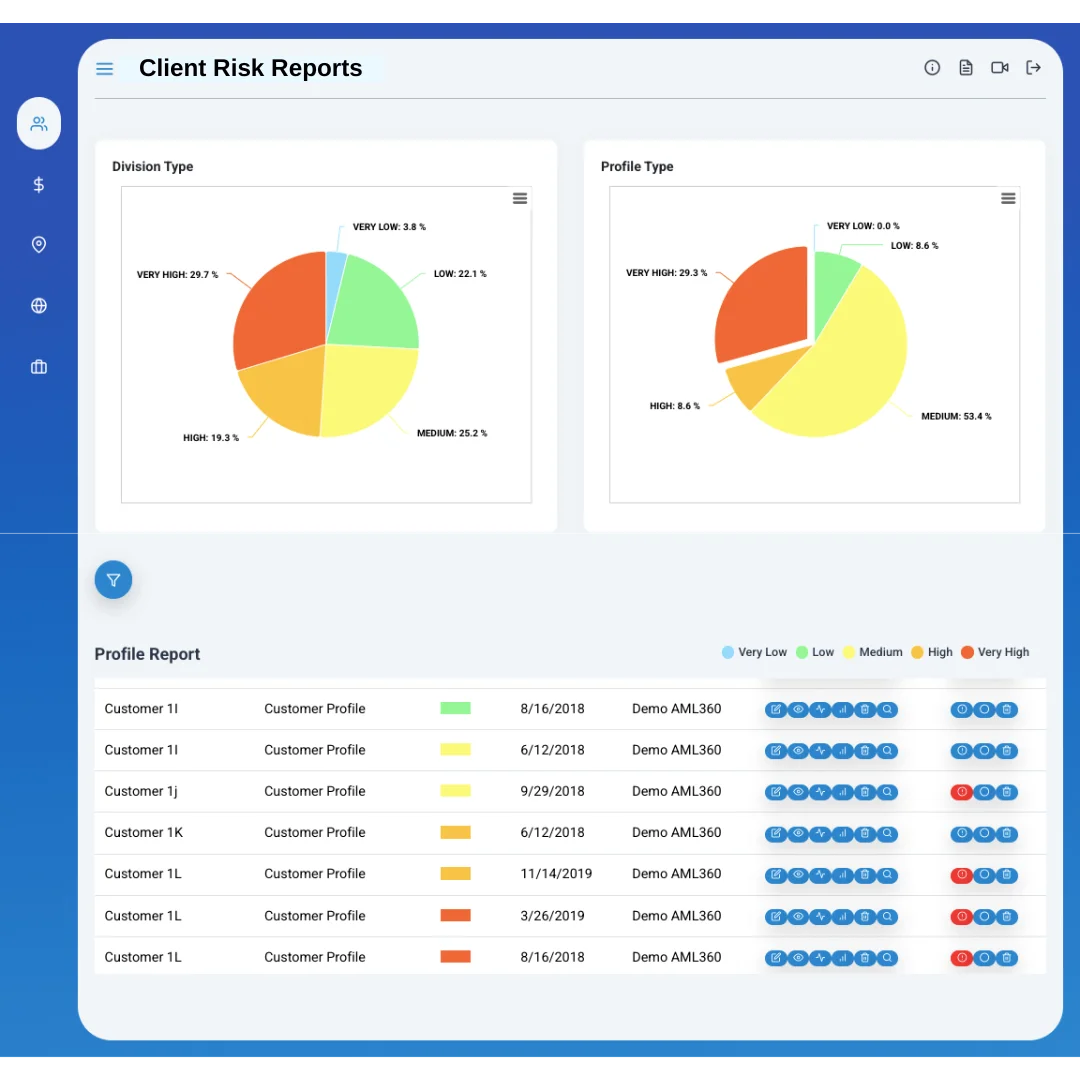

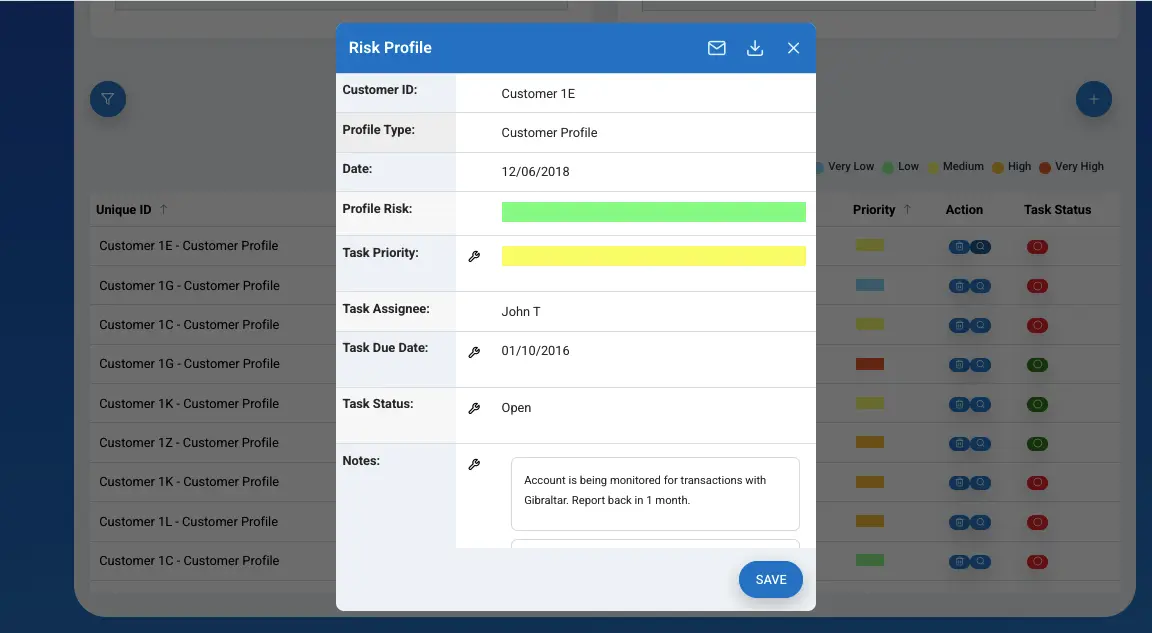

We provide you a compliance report on the AML customer risk rating methodology as a supporting document to your AML/CFT Programme.

Not only can we assist in the development of an AML customer risk rating and scoring methodology, but we can also provide reporting services.

Our AML customer risk rating and reporting options can be through PDF, online compliance registers or both.

We ensure integration is quick and affordable.

Don’t leave the AML customer risk rating obligation on the back-burner. Avoid the risk of a regulatory fine and govern your AML customer risk rating model with AML360™.

Get confident by using services that have ongoing oversight of AML/CFT compliance professionals.

More Info – AML Customer Risks