New Zealand’s Anti-Money Laundering compliance laws are referred to risk-based legislation or law that applies risk-based principles. This means decision making arising for AML/CFT compliance needs to be based on informed knowledge and be relevant to the risk exposure.

By establishing systems for risk-based reporting, a business is better equipped in implementing an AML/CFT compliance programme to manage the risk level presented. However money laundering and terrorism financing risks are not stagnant. Systems in place for risk profiling, monitoring and reporting therefore need to be flexible and be able to modify and align as underlying risk parameters or thresholds change.

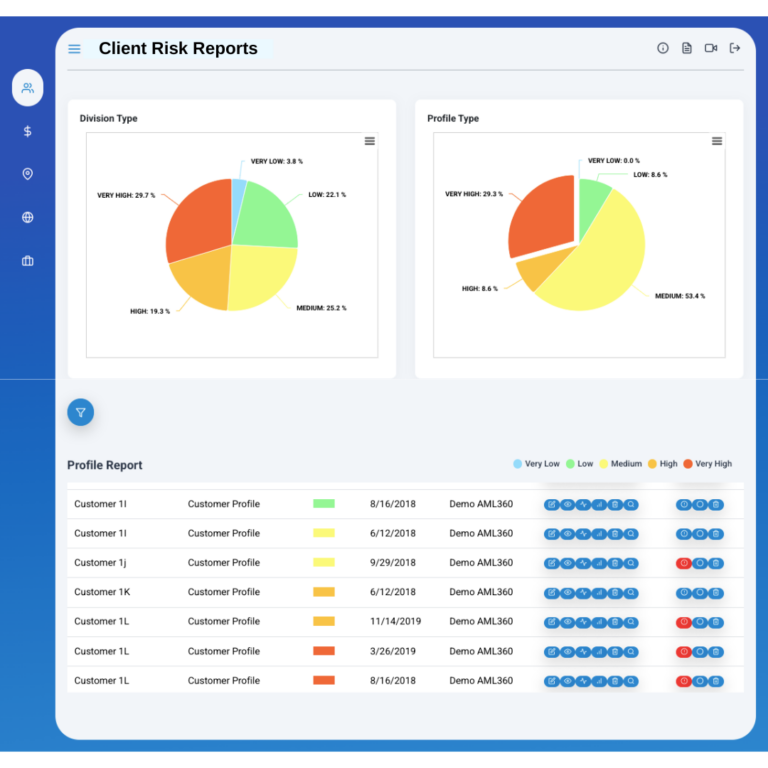

The AML customer risk rating or AML customer risk score will therefore assist the business to make decisions on resourcing commitments to manage the customer risk.

The customer risk report will inform the business and the Anti-Money Laundering Compliance Officer on the frequency of reporting for client activity. The customer risk report will also inform on the reasons why the risk is low, medium or high.

In having informed knowledge of AML customer risk rating, the business is able to demonstrate compliance for application of enhanced due diligence. Section 22(1)(d) of the Anti-Money Laundering and Countering Financing of Terrorism Act (AML/CFT Act), requires enhanced due diligence on higher risk customers. If a business cannot demonstrate how they make decision making on higher risk customers, then they cannot demonstrate compliance with section 22(1)(d).

To achieve AML customer risk rating and scoring, a business will need to start with examining the type of data that exists relevant across all customers and/or the majority of customers.

The data will then need to be examined for relevance to ML/FT risks. This may include information of the country or countries linked to the client either by being domiciled or reach of business activity.

The expected volume of the customer activity and the expected value of the customer activity is also relevant to segregating risks levels.

The types of products or services that the customer accesses should be included in the AML customer risk rating, including the method of interaction with the client.

Where some customers have data gaps, an automatic default of high should be applied to that data gap. Once the ‘missing’ information is gathered, the client’s profile can be updated for the AML customer risk rating model.